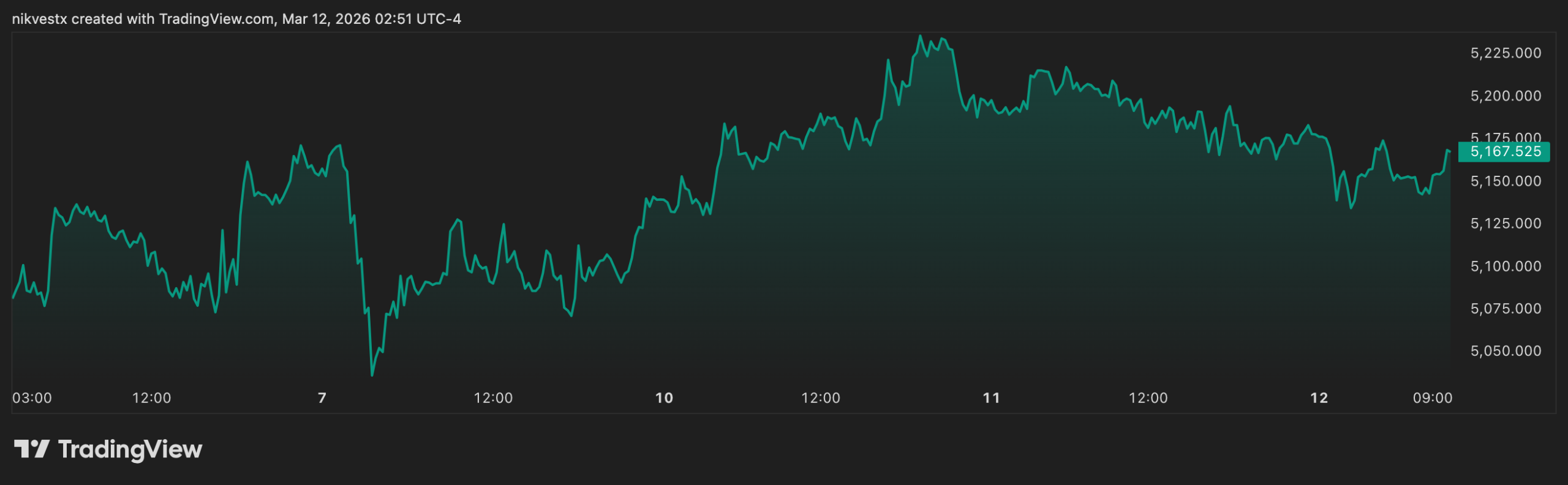

🥇 Gold's Safe-Haven Rally Smothered by Dominant Dollar

March 12, 2026

Physical Dominance: Architecting the Geopolitical Fracturing of Global Commodities

Let’s diagnose a fundamental shift in the 2026 macroeconomic landscape. For the last decade, investors have been obsessed with “Digital Scarcity” and software-driven multiples. Today,

The Macroeconomic Repricing: Crude Volatility, Gold’s Critical Test, and the Return of Dollar Supremacy

Let’s diagnose a massive structural shift currently shaking the global markets. Retail operators are getting whipsawed by sudden drops in crude oil and precious metals,

Gold Records Worst Week in Decades

Precious metals are taking a massive hit as geopolitical fears ironically fail to outweigh shifting rate cut bets. Gold prices extended a vicious losing streak

Gold Plunges 9% Defying War-Time Logic

The ultimate safe haven is acting like a risk asset as rates crush bullion appeal. Gold plummeted to roughly $4,556 per ounce, wiping out

Forecast and Strategic Assessment: Global and Regional Trajectories Following the Decapitation of the Iranian Regime

The geopolitical architecture of the Middle East, and by extension the broader international system, has reached a profound and irreversible inflection point following the unprecedented

The Structural Decoupling: Trading the $6,200 Gold Regime Shift in 2026

🥇 Gold’s Safe-Haven Rally Smothered by Dominant Dollar March 12, 2026 Gold will face intense algorithmic selling pressure every time it tests local highs against

The $5,205 Breakout: Trading the Tariff Panic and the Geopolitical Safe-Haven Supernova

Retail traders are staring at a five-day vertical streak in gold, watching it smash through $5,180 to tag $5,205 intraday, and they are desperately waiting

The Fear Premium: Why US-Iran Brinkmanship Just Broke the Golden Rule

When the drums of war beat loud enough, the fundamental laws of finance temporarily cease to exist. Textbooks tell you that when the US Dollar

The 2025 “Divergence” Report

2025: The Year the Market Sold ‘The Future’ to Buy ‘The Periodic Table’. 1. Silver (+130%): The “Industrial Squeeze” of the Century Status: Asset of

Forex & Commodities: The Monday Gap

1. Gold’s “Safe Haven” Premium While crypto bleeds, the yellow metal is holding the line at $4,300. Gold (XAU/USD) is currently trading at $4,337.85, pushing

Global Macro: The “Peace Shock” & The Golden Hedge

1. Crude Oil (WTI): The Geneva Peace Talks Crash Peace is profitable for humanity, but catastrophic for oil bulls. WTI Crude has plummeted to $58.00

Forex & Commodities Pulse: Riding the Waves of Uncertainty in Late 2025

As we hit November 21, 2025, the forex and commodities arenas are a whirlwind of shifting sentiments. The US Dollar is clawing back ground amid

The $4,000 Crossroads: Deep Analysis of Forex, Commodities, and Macroeconomic Tides

The current market sentiment is generally risk-off, driven by persistent macroeconomic uncertainty, hawkish signals from the Federal Reserve, and geopolitical tensions. This has led to strong dollar performance, pressure on commodities like Gold and Oil, and a deep correction in the high-momentum Tech and Crypto sectors.

Forex & Commodities: The Age of Strategic Divergence

The market narrative for November 2025 is one of profound and irreversible divergence. We are witnessing a “Great Un-mooring,” where asset classes are no longer

Forex & Commodities: USD Strength and Geopolitical Twists Redefine the Landscape

The world of currencies and raw materials feels like a high-stakes game these days, with the dollar’s comeback throwing shade on everything from gold to

Major Forex & Commodities News | November 12 2025

Just as the market priced in “higher for longer,” a key Fed official just reignited hopes for a December rate cut, sending the Dollar tumbling.

Major Forex & Commodities News | November 11, 2025

1. Gold’s Hyperdrive: The $4,100 Breakout Is Here The government shutdown is ending, and the dollar is stumbling. Gold just hit the ignition switch. Gold

Trading GOLD (XAU/USD) in October 2025: Forecasts, Trends, Signals & Predictions

Table of Contents Introduction: Why Gold Dominates Global Market Sentiment Discover how gold’s ancient allure translates into a modern barometer for global economic health, influencing

September 2025 Forecast, Analysis and Price Predictions: XAU/USD (Gold)

1. Introduction: The Enduring Importance of Gold in September 2025 As we navigate the complexities of the global financial landscape in September 2025, gold (XAU/USD)

Gold (XAU/USD) August 2025 Forecast: Expert Strategies & Insights

Gold (XAU/USD), the premier safe-haven asset, remains a cornerstone of commodities trading, reflecting global economic uncertainties and monetary policy shifts. As we approach August 2025,